Bevan Goldswain/E+ via Getty Images

4D Molecular Therapeutics, Inc., also known as 4DMT (NASDAQ:FDMT), is a clinical-stage biotechnology company that leverages its Therapeutic Vector Evolution platform to innovate genetic medicine. This technology designs specialized viral vectors that are precision tools for gene delivery across various types of cells and organs. FDMT’s pipeline is focused on ophthalmology, pulmonology, and cardiology, with promising clinical outcomes for 4D-150 for wet AMD progressing to Phase 3 and 4D-710 for Cystic Fibrosis treatment. These advancements showcase the platform’s efficacy and enhance FDMT’s market value by progressing key revolutionary genetic therapies. This enables FDMT to research and quickly produce many potential gene therapy drug candidates. So, despite the inherent biotech risks, I believe FDMT is a great investment in the sector at these levels.

Platform IP: Business Overview

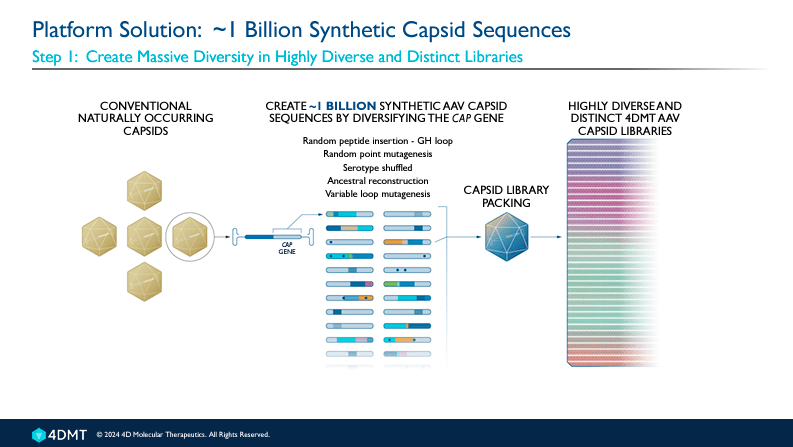

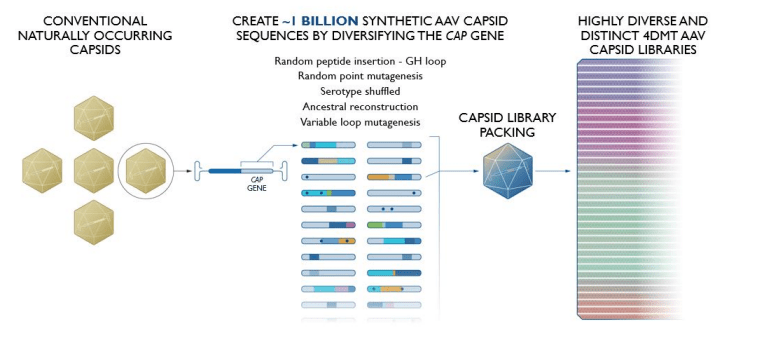

FDMT is a clinical-stage biotechnology company focused on designing and developing targeted genetic medicines using a method known as “Directed Evolution.” This method involves testing and selecting viruses as carriers or vectors for delivering gene therapies. FDMT has a proprietary platform, Therapeutic Vector Evolution, which creates custom viral vectors by transforming natural viruses into engineered tools to deliver therapeutic genes to specific cells or tissues in the liver, retina, heart, brain, skeletal muscles, and lungs for treating several diseases. Therapeutic Vector Evolution leverages directed evolution to create synthetic capsids tailored for specific disease treatments, which I believe is what sets FDMT apart from the pack.

Source: 4DMT Corporate Presentation. April 2024.

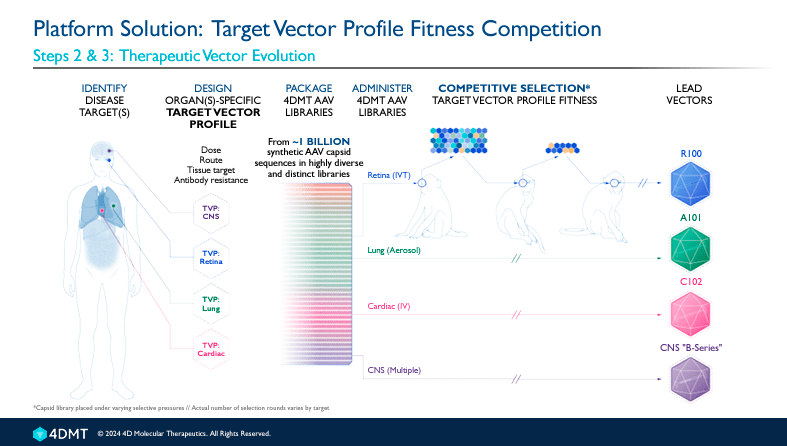

The platform can generate synthetic capsids that best match the Target Vector profile [TVP], which defines the type of cells the medicine directs to. A capsid is a protein shell located around a virus’s nucleic acid (DNA or RNA). It helps the virus invade host cells to deliver its genetic material. The capsid structures protect the viral genetic material from degradation and facilitate the virus’s penetration of the target cell’s membranes.

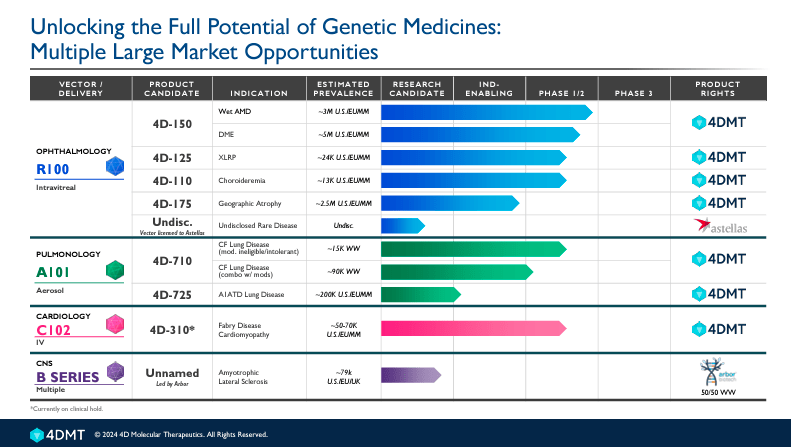

FDMT’s broad pipeline includes three therapeutic areas: ophthalmology, pulmonology, and cardiology. The product candidates are administered intravitreally in the ophthalmology programs using R100 as vector delivery. This program presents 5 product candidates. Overall, 4D-150, 4D-125, and 4D-110 are in phase 1/2 studies, 4D-175 is a research candidate preparing to be IND-enabling, and an additional undisclosed product is also in the early preclinical research stage.

Product Pipeline Details: Breakdown

Concretely, 1) 4D-150 has two indications: Wet Age-Related Macular Degeneration [AMD] and Diabetic Macular Edema [DME]. These are serious eye conditions that can lead to vision loss if untreated. Wet AMD is a leading cause of vision loss in older adults. The current treatment involves injections in the eye to inhibit the growth of abnormal blood vessels. 4D-150 offers a long-lasting solution that delivers gene therapy to the retina to produce therapeutic proteins to combat the disease. DME is a complication of diabetes that produces swelling in the macula due to leaking blood vessels in the retina, causing blindness in diabetes patients. Current treatments involve eye injections similar to those used in Wet AMD or laser surgery to reduce swelling and prevent further vision loss. 4D-150 provides a new gene therapy approach that produces prolonged relief and sustained benefits.

Source: 4DMT Corporate Presentation. April 2024.

FDMT also has 2) 4D-125, which targets X-linked Retinitis Pigmentosa [XLRP]. XLRP is a severe form of Retinitis Pigmentosa [RP], a genetic disorder primarily affecting males, that induces progressive vision loss due to the degeneration of photoreceptor cells in the retina. 4D-125 aims to deliver a functional gene to the retina to correct the underlying genetic defect that provokes XLRP. This medicine promises hope that the vision loss can be halted or even reversed, addressing the root cause instead of only managing symptoms therapies.

Moreover, the company’s 3) 4D-110 is an application for Choroideremia. Choroideremia is caused by mutations in the CHM gene, which lead to the degeneration of the choroid, retinal pigment epithelium, and photoreceptors in the eye. 4D-110 delivers a functional copy of the CHM gene into the retina to improve visual outcomes in patients with limited current treatment options.

Lastly, FDMT has 4) 4D-175, intended for Geographic Atrophy, an advanced form of age-related macular degeneration (AMD). Geographic Atrophy involves the progressive degeneration of the retinal pigment epithelium, photoreceptors, and choriocapillaris, primarily in the macula, leading to severe vision loss and blindness in elderly patients. The 4D-175 medicine delivers therapeutic genes directly to the retinal cells to slow the disease’s progression and restore visual function. FDMT acquired sCFH as payload for 4D-175 from Aevitas Therapeutics to enhance its therapeutic potential by providing a critical component for the drug’s action mechanism. The last one is a 5) undisclosed drug with a vector licensed to Astellas for unrevealed Rare Monogenic Ophthalmic Disease.

Source: 4DMT Corporate Presentation. April 2024.

Furthermore, FDMT’s pulmonology therapeutics are products administered using aerosol methods with A101 as vector delivery. The product candidates in this category are 4D-710, indicated for two diseases: Cystic Fibrosis [CF] not modulator—amenable and CF modulator—amenable (both in phase ½). CF is a genetic lung disorder that affects the lungs, pancreas, and other organs. This leads to respiratory and digestive disorders caused by mutations of the CFTR gene, which encodes the cystic fibrosis conductance regulator protein that controls the movement of salt and water in and out of the cells. FDMT’s modulators help improve the protein’s function on the cell surface, aiming to restore normal function regardless of whether the specific CFTR mutations. This is significant because it addresses a major limitation of current CF treatments. Thus, the drug aims to deliver a functional copy of the CFTR gene into the cells, potentially restoring normal function instead of modulating the dysfunctional CFTR protein. The other drug candidate in the pulmonology program is 4D-725, which addresses Alpha-1 Antitrypsin [A1AT] Deficiency Lung Disease and is a research candidate.

It’s worth noting that FDMT’s cardiology category has a single product, 4D-310. This one is administered intravenously for Fabry Disease and is in phase 1/2. This condition is a genetic disorder characterized by the buildup of a particular type of fat globotriaosylceramide [Gb3] in the body’s cells. This accumulation can lead to a variety of symptoms, including pain, kidney failure, heart disease, and stroke. The treatment delivers a functional copy of the gene, which is deficient in patients with this disease. Typically, the GLA gene produces an enzyme that breaks down Gb3. By introducing a working version of this gene, 4D-310 restores the enzyme’s activity levels and reduces the accumulation of Gb3.

Finally, FDNT’s Central Nervous System [CNS] program presents an early-development drug candidate for Amyotrophic Lateral Sclerosis [ALS] in partnership with Arbor Biotechnologies. ALS is a progressive neurodegenerative disease that affects brain and spinal cord cells, leading to loss of muscle control. This research is subject to a B series funding to expand investigation capabilities, but is currently in the exploratory phase.

FDMT’s Evolutionary Leap in Gene Therapy

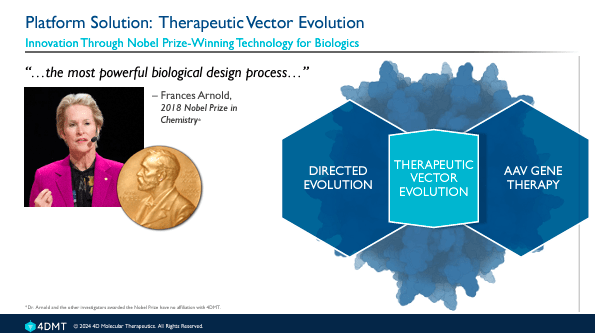

I believe FDNT’s main value drive lies in its Therapeutic Vector Evolution platform. In fact, this is an application of Nobel Prize-winning technology for biologics. The 2018 Chemistry Nobel Prize winner, Frances Arnold, described evolution as “the most powerful biological design process.” FDMT’s vector evolution leverages these inherent adaptive dynamics, making its technology particularly promising. So far, FDMT’s positive results corroborate its efficacy. This is promising from an investment perspective, as it’s a sign that the underlying technology has a solid body of research rather than a highly speculative novel approach.

Source: 4DMT Corporate Presentation. April 2024.

For instance, in phase 2 clinical trials, 4D-150’s PRISM study for wet AMD, outcomes enabled rapid advancement towards phase 3 (expected for Q1 2025). Furthermore, 4D-710 received the Rare Pediatric Disease Designation from the FDA after obtaining encouraging results in phase 1/2 clinical trials, including improved CFTR expression and pulmonary function in patients. Further updates on the AEROW study and pivotal trial should arrive relatively soon, as they were expected for Q1 2024.

Another great example of FDMT’s promising platform was 4D-310 for Fabry Disease Cardiomyopathy, which had positive interim data presented at the WORLDSymposium in February 2024. The drug demonstrated clinical symptom improvements, robust and durable delivery, and transgene expression. Overall, I believe these results validate the robustness and versatility of FDMT’s platform and pipeline in gene therapy.

Strong Buy: Valuation Analysis

From a valuation perspective, FDMT trades at a $1.20 billion market cap. This is relatively big for a company without a phase 3 drug candidate, but FDMT isn’t your typical biotech company. FDMT’s main value driver is its platform and drug development approach through evolution mechanisms. The company’s ability to use its AAV capsid libraries and test them in animals to find the lead vectors for different disease targets is groundbreaking. Theoretically, I believe this approach will give FDMT a relatively high drug candidate throughput for gene therapies that will likely require a single administration if approved. So, based solely on this massive differentiating factor, I believe FDMT’s valuation seems quite reasonable, if not cheap.

Source: FDMT’s 2023 10-K.

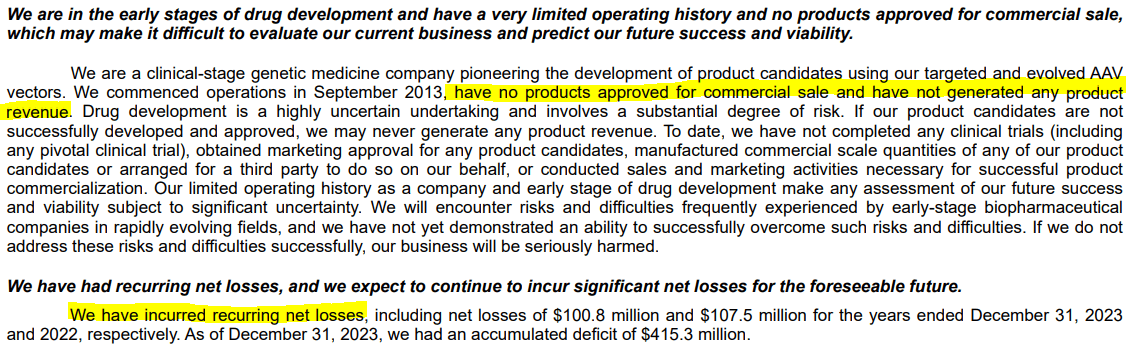

Moreover, FDMT recently raised an additional $300 million in a public offering, which should considerably increase its cash reserves. As of December 2023, FDMT had $249.1 million in cash and $39.1 million in marketable securities. The company’s cash and equivalents should be approximately $588.2 million post-raise. I estimate its latest quarterly cash burn was roughly $25.2 million, which implies a yearly cash burn of $100.8 million. I obtained this figure by adding the latest quarterly CFOs and Net CAPEX. Thus, FDMT’s cash runway post-raise should be about 5.8 years, which is quite healthy and should be enough to fund its research through an eventual FDA approval. Also, it’s worth noting that FDMT only has $32.1 million in total liabilities and no financial debt.

Additionally, FDMT now effectively trades at approximately two times its cash and equivalents, which denotes relatively good value for investors. Moreover, if we add the $300 million to its December 2023 book value, FDMT’s equity should be about $607.8 million, implying a P/B ratio of 2.0. This multiple also seems undervalued compared to its sector median P/B multiple 2.2. So, I think it’s reasonable to conclude that FDMT trades at a compelling valuation, especially in light of its groundbreaking platform and upcoming Phase 3 drug candidates 4D-150 and 4D-710.

Still Highly Speculative: Risk Assessment

Naturally, FDMT is not without its risks. Particularly, I think that this novel platform is well grounded in evolutionary mechanisms that are relatively well understood, but it’s still undoubtedly a novel approach with unique risks. For instance, production issues and public perception hurdles could hamper FDMT’s prospects. Moreover, the FDA and EMA have raised concerns regarding the registrational path of 4D-710, and could foreshadow future regulatory setbacks.

Source: FDMT’s 2023 10-K.

Moreover, FDMT still has no product revenues and has only accumulated losses. Since FDMT’s drug candidates have no Phase 3 clinical trials yet, there’s still substantial uncertainty about the ultimate viability of its technology when tested in larger populations. If Phase 3 trials show that FDMT’s underlying approach isn’t as safe or effective as initially thought, the stock could quickly depreciate as all its drug candidates share the same fundamental mechanics. But despite these risks, I believe FDMT’s potential could be substantial, particularly if it gets FDA approval for any of its two leading drug candidates (4D-150 and 4D-710), as it would validate their platform’s effectiveness and, by extension, its long term business viability. Since FDMT has enough resources for the foreseeable future, I believe it’s a “strong buy” for investors willing to accept these uncertainties.

Source: TradingView.

A Hidden Gem: Conclusion

FDMT’s main value driver is its platform, which I believe is its key differentiator from other biotech companies. This enables FDMT to research and quickly produce many potential gene therapy drug candidates. If it gets a single FDA approval for any of them, it would essentially validate its underlying technology by extension, immediately unlocking substantial shareholder value beyond the FDA approval itself. So far, 4D-150 and 4D-710 are FDMT’s leading candidates, and they will soon start Phase 3 clinical trials, so the finish line is within sight. Naturally, risks are embedded in this equation, but are mostly typical for all biotech investments. However, the potential for FDMT’s platform to revolutionize gene therapy, combined with positive interim clinical trial results and a solid financial runway, supports a favorable outlook. Hence, I think FDMT is a fantastic opportunity for investors who understand the inherent risks.